Dyness Knowledge | Commercial and Industrial Storage Returns Amidst Policy Shifts: The Transition from Peak Shaving and Valley Filling to a Multidimensional Revenue Matrix

-

Technical Blog

-

2026-04-17

2026-04-17 -

Dyness

Dyness

Since 2025, with the gradual abolition of mandatory energy storage requirements for new energy projects at the national level and the accelerated nationwide rollout of electricity spot markets, the traditional peak-valley arbitrage model for commercial and industrial energy storage has faced a dual challenge: shrinking profit margins and intensifying homogeneous competition. The industry is currently evolving from a mere "peak-shaving and valley-filling tool" into a "power asset capable of participating in multiple market transactions." The core of this transformation lies in establishing a revenue framework—through technological upgrades and the restructuring of operational models—that encompasses a diverse range of electricity market mechanisms.

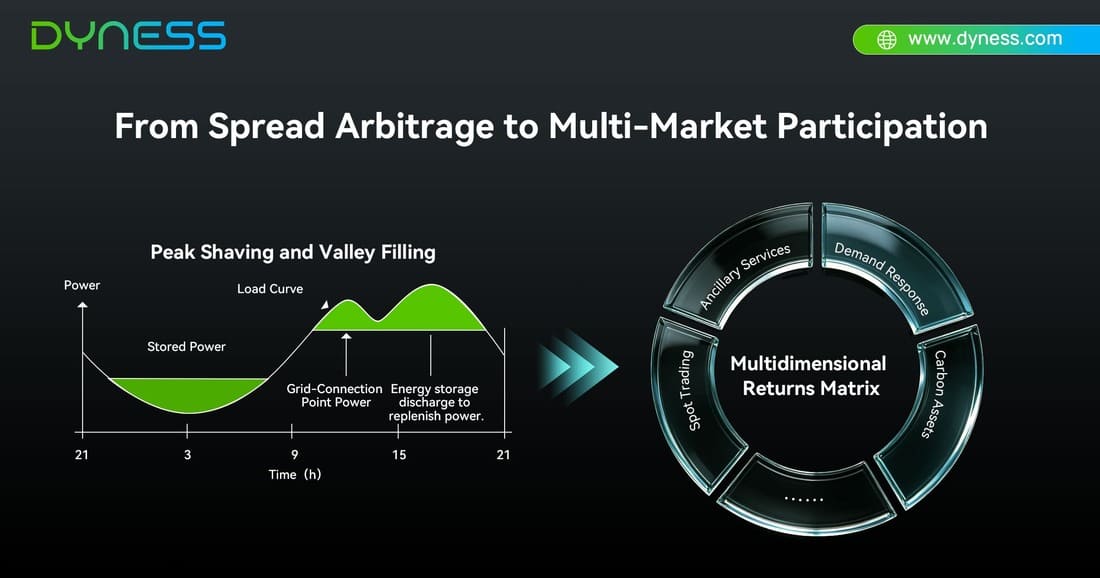

Restructuring the Profit Logic: From Price Arbitrage to Multi-Market Participation

Changes at the policy level fundamentally constitute a redefinition of the role of energy storage. With the phasing out of mandatory storage mandates, energy storage is no longer merely an ancillary component of new energy projects; rather, it has emerged as a market entity possessing its own independent logic for investment returns. Concurrently, the pathways for independent storage facilities to participate in mechanisms such as spot markets, ancillary services, and demand response are becoming increasingly clear, leading to a diversification of revenue streams.

Based on actual operational performance, the limitations of a standalone peak-valley arbitrage model are becoming apparent:

Peak-valley price spreads are narrowing across multiple provinces, with spreads in some regions shrinking by approximately 20%–30%.

The annual utilization hours for energy storage systems remain low; typical projects undergo fewer than 300 cycles per year.

The investment payback period is being involuntarily extended.

Against this backdrop, the revenue models for energy storage projects are shifting toward a "portfolio-based structure," the core components of which include:

Peak-to-off-peak arbitrage (base revenue).

Demand response (capacity payments + dispatch subsidies).

Ancillary services (peak shaving, frequency regulation, reserve power, etc.).

Electricity spot trading (arbitrage based on price fluctuations).

Green electricity and carbon assets (supplementary revenue).

The essence of this multi-dimensional revenue structure is to transform energy storage from a "load management device" into a "power market participating unit."

Technology-Driven: The Foundation for Realizing Multiple Revenue Streams

For industrial and commercial energy storage systems to achieve profitability through diversified revenue models, innovation in business models alone is far from sufficient; technical capability serves as the fundamental underpinning. Specifically, dispatch precision, response speed, and system stability constitute the three core technical pillars.

The first key factor is scheduling capability. Historically, operations relied heavily on heuristic strategies and fixed charging/discharging rules, often proving ineffective in responding to fluctuations in electricity prices. The current trend involves utilizing predictive models to make forward-looking assessments of 15-minute-interval load profiles and spot market electricity prices, thereby dynamically optimizing charging and discharging strategies. Fundamentally, this entails a multi-objective optimization process that balances revenue maximization against battery degradation—specifically, enabling the system to make autonomous decisions regarding whether to engage in deep charging/discharging cycles or to participate in frequency regulation markets to generate additional revenue. The effectiveness of these scheduling strategies directly determines the revenue generated per unit of electricity.

The second key factor is grid-forming capability. As the penetration rate of new energy sources rises, fluctuations in grid voltage and frequency have intensified significantly. Traditional energy storage systems are grid-following devices; they rely on external grid signals to respond and therefore possess limited flexibility. Grid-forming energy storage systems, conversely, possess the autonomous capability to support the grid; they can emulate the characteristics of synchronous generators, providing inertial response, primary frequency regulation, and even black-start services. Only by possessing grid-forming capability can commercial and industrial energy storage systems qualify to participate in ancillary service markets—such as frequency regulation, reserve capacity, and local grid support—without which they would be unable to generate revenue from these sources.

Finally, there is the balance between service life and financial returns. When engaging in multi-market trading, one must not focus solely on short-term gains; instead, a cost-benefit assessment should be conducted from a full lifecycle perspective. Battery degradation follows predictable patterns: every charge-discharge cycle accelerates aging, and even during periods of inactivity, the calendar life continues to deplete. The rational strategy is to discharge decisively during periods of high electricity prices, while adopting a "shallow charge, shallow discharge" approach during low-yield windows to avoid unnecessary deep cycling. By systematically coupling charge-discharge strategies with battery degradation models—even if the profit from a single transaction may be slightly reduced—the Levelized Cost of Electricity (LCOE) is lowered over the full lifecycle. This achieves the dual objective of "extended service life and maximized total returns"—a concept that can be summarized as the "healthy operation" logic of energy storage: trading minimal degradation for long-term economic viability.

Through system-level optimization, battery lifespan can be extended while simultaneously reducing the Levelized Cost of Electricity (LCOE) over the entire lifecycle, thereby enhancing overall profitability.

Scenario Implementation: An Engineered Pathway to Multidimensional Returns

Ultimately, technical capabilities must translate into tangible returns through specific use cases.

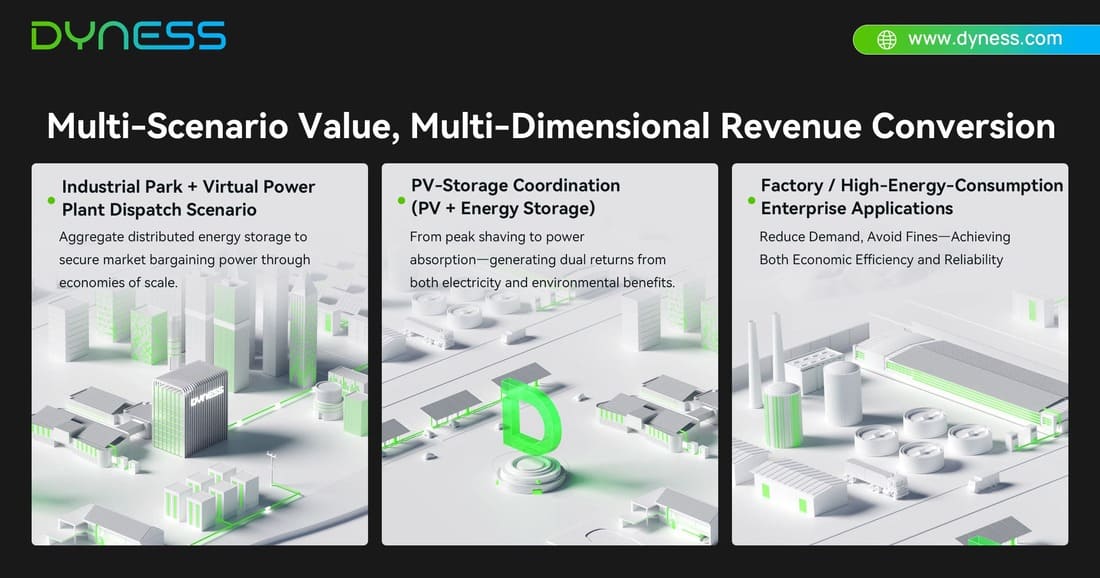

Scenario 1: Park-Level Aggregation and Virtual Power Plants

By aggregating multiple distributed energy storage units, a dispatchable resource pool capable of achieving economies of scale can be established. Typical implementation pathways include connecting to a unified dispatch platform, developing models for dispatchable capacity, integrating with demand response and spot markets, and executing centralized bidding and dispatch operations. Compared to the operation of individual standalone stations, the aggregated system demonstrates superior dispatch stability, enhanced market bargaining power, and higher overall revenue levels.

Scenario 2: Synergistic Integration of Solar and Storage, and Green Power Absorption

In regions with a high penetration of distributed photovoltaics, the core function of energy storage is shifting from "peak shaving" to "grid integration optimization." Specifically, this entails increasing the rate of PV self-consumption, mitigating curtailment and export limitations, and participating in green electricity trading to capture price premiums. When integrated with carbon market mechanisms, energy storage can also indirectly contribute to the accounting of carbon emission reductions and the trading of carbon assets, thereby establishing a dual-revenue structure comprising both "electricity revenue" and "environmental revenue."

Scenario 3: Demand Management for High-Energy-Consumption Enterprises

In industrial settings where two-part tariffs are in effect, demand charges typically constitute a significant portion of electricity costs. The primary role of energy storage in such contexts lies in reducing peak demand, smoothing load profiles, and avoiding penalties for exceeding demand limits. Furthermore, energy storage can serve as a backup power source, thereby enhancing production continuity. This combined value—encompassing both economic efficiency and reliability—is particularly pronounced in energy-intensive industries.

Competitive Barriers: From Equipment Sales to Operational Capabilities

As the industry enters a phase of intense competition, relying solely on equipment pricing to achieve differentiation is no longer viable. The core of future competition will center on the following key areas.

1. Business Model Capabilities

These include Energy Storage as a Service (EaaS), revenue-sharing mechanisms, and Energy Management Contracts (EMC)—approaches that fundamentally transform one-time capital investments into long-term operational returns, thereby enhancing project implementation rates.

2. System Integration and Security Capabilities

The critical factors are: battery system safety design (thermal runaway protection), fire protection and monitoring systems, and alignment with grid connection and communication standards—safety and regulatory compliance will serve as the baseline requirements for the project's long-term operation.

3. Data and Operational Capabilities

The core assets of future energy storage extend beyond the equipment itself to encompass operational data and dispatch capabilities—specifically, unified multi-site dispatch, continuous strategy optimization, and iterative revenue modeling. Ultimately, whoever can operate these assets most efficiently will secure the most stable returns.

Conclusion: Moving from "Price Competition" to "Value Competition"

Against the backdrop of gradually diminishing policy incentives, the commercial and industrial (C&I) energy storage sector is undergoing a structural transformation. In the short term, narrowing peak-to-off-peak price spreads are compressing traditional profit margins. However, from a long-term perspective, the maturation of multi-market mechanisms is unlocking a broader scope of value for energy storage. It is foreseeable that industry differentiation will intensify further in the future; projects relying on a single arbitrage model will be gradually phased out, while systems equipped with multi-market participation capabilities and intelligent dispatching capabilities will emerge as the mainstream.

The fundamental nature of energy storage is shifting from a "cost center" to a "revenue-generating asset." The key to this transformation lies not in scaling up operations, but rather in a deep understanding and synergistic application of technology, use cases, and market mechanisms.

Dyness Digital Energy Technology Co., LTD

WhatsApp: +86 181 3643 0896 Email: info@dyness-tech.com

Address:7th–8th Floors, Building 3 No. 58 Nanhu Road Chengnan Subdistrict, Wuzhong District Suzhou, China

Dyness Website: https://www.dyness.com/

Dyness community: https://www.facebook.com/groups/73560020090